Wayfair-you’ve got just what I don’t need

I doubt there’s a more common question that I get from business owners that sell a product than -“How does the Supreme Court Wayfair decision affect me collecting sales tax from the products that I sell outside of Georgia?”

Books have been written on this, but the short version is that until the recent Supreme Court decision, charging sales tax was governed by whether you had Nexus (a tax term meaning a physical office, employee, or presence in a state) and was fairly simple to determine. We’ve seen this coming for a while and, in 2017, wrote this blog post to give some guidance:

Do you have a Nexus?

It’s not a new car, but a business presence. How Operating across state lines presents tax risks — or possibly rewards

Well since that time, the states have grown an insatiable lust for your dollars and have alleged that even making a sales call (via phone) is equivalent to having a Nexus in their state. Some of us can remember when sales on Amazon didn’t have sales tax added. The Supreme Court case (see below) introduced a new (i.e. tax-increasing) concept for the government called economic nexus. For the most part, it destroys the physical presence test that has been tax law for decades.

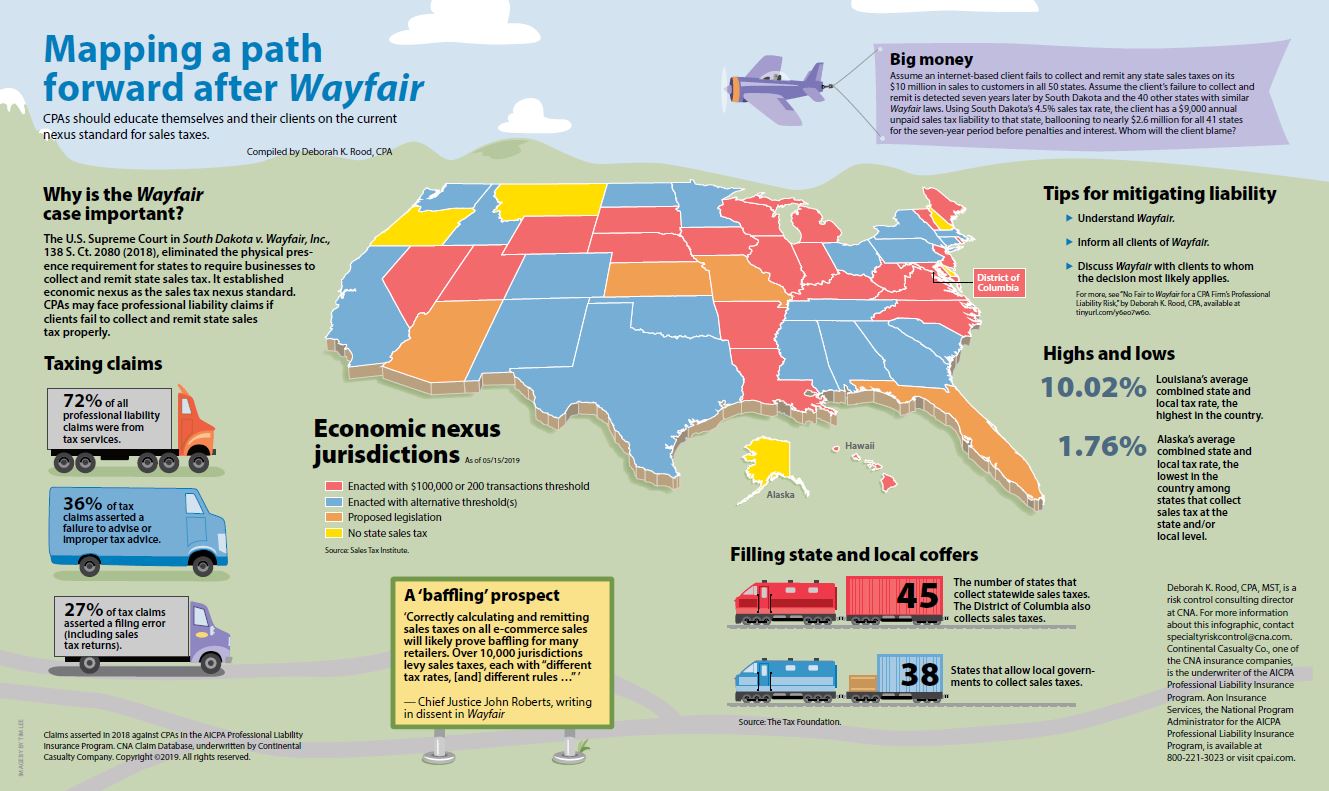

The picture below will help you follow the timeline.

The far-reaching effects are beyond one blog post, so be sure to contact us in you need to discuss this aspect of your business.